Rethink° September

How to Blow Up an Economy, Centralized Tokenization, and climate risk insurance for humanitarian action

We’ll start this episode with a personal note. To skip it, jump to the next paragraph 😉. We would need your help for some end-of-the-summer motivation boost. Every time we have a new subscriber, we get this motivation boost. So help us trigger that and share this newsletter with one person that you think will enjoy it. Thanks a lot and…

…let’s get into it

How to Blow Up an Economy

📹 Teaser: When everyone else calls for economic growth, innovation, and addition, Timothée Parrique demands demolition, sabotage, and removal. Our strive towards infinite growth is not sustainable on a finite planet. So far, no economy in the world has managed to grow its economy without overshooting the planetary boundaries. That’s why we need an economic strategy based on subtractions, not additions. And we need to rethink the economy's purpose, as growth tells us nothing about prosperity and well-being. So, is de-growth the solution? Watch now → (14 min)

🤔 Moritz’ two cents: I like the ideas of Parrique, and he is dropping very hard facts in this video. Certainly worth to watch it (which is why it’s on this Newsletter 🎁). I feel he is becoming the poster-researcher for the degrowth movement and as you have probably read, I am very open towards the idea of degrowth. At the same time, when starting the video, I thought that we shouldn’t sell the idea of degrowth as “too radical”. I do not think degrowth has to be radical, most people might even benefit from it, also in the short run. In the end, it is a concept made for the people. But the arguments in favour will need to be comprehensible and well sold because the lobby against it is rich, accordingly powerful. Because the once hurt most by a degrowth-done-right movement will be the luxury lifestyles of the richest 1%.

Anyway, as the video goes on, he delivers many nice metaphors that you will be able to take away and use for your own pro-degrowth arguments. Here is one: “If you want to lose 20 kg, you can do a diet, or chop one of your legs off. In terms of Kilogram it’s all the same, in terms of wellbeing the one is clearly better than the other. That is the choice we have today: Plant degrowth (the diet) today, or wait for the planetary collapse tomorrow.”

And I am in love with his closing statement about a future economy: “Poorer in money, but richer in time and connection” 🕥. Even if you do not agree with his full final statement (which I also do not do 100%), we might agree that the direction is correct, and we can pan out the details later.

Lego abandons effort to make bricks from recycled plastic bottles

📰 Teaser: Lego has stopped a project to make bricks from recycled drinks bottles instead of oil-based plastic, saying it would have led to higher carbon emissions over the product’s lifetime.

🤔 Max’s two cents: As disliked as plastic is by now, its controlled material properties and low resource footprint, including carbon, make it challenging to replace easily with bio-based alternatives. This holds especially true when considering the lifecycle footprints of all available options. Ultimately, it is the consideration of the whole lifecycle of a product that matters. This case study about LEGO Group is rather insightful for its two takeaways:

First, rely on lifecycle assessment where possible to inform sustainability management.

Second, aim for a reduction in resources and materials used. Green growth is a myth on a finite planet, as uncomfortable as this realization is.

Regarding changing complex systems such as our current socioeconomic one, “quick fixes” do not exist. This challenge and its complexity should, however, not discourage us, as a portfolio of actions addressing different aspects of our sustainability challenges will lead to meaningful change in due time.

Parts of America are becoming uninsurable

📰 Teaser: While Americans moved to risky places, climate change made them even more risky. Private insurers are now raising alarm bells. Firms are writing fewer policies in vulnerable areas and are withdrawing from some states altogether. A new report from the First Street Foundation, a non-profit research group, suggests that 6.8 million people have experienced increased rates or canceled policies due to rising flood, wind, or wildfire risk. Another 39 million properties, or approximately a quarter of all properties in the continental United States, are still subject to climate risks that have yet to be reflected in their premiums. Continue Reading → (11 min)

🤔 Max’s two cents: The insurance industry makes for a good indicator of future climate impacts and our understanding of those. Its foundational business model necessitates using the latest scientific findings and accurate statistical analysis, irrespective of political leaning, personal preferences, or any other factors that hamper and muddle debates around climate change. The findings of this report are instructive beyond the U.S. as it highlights how critical implicit subsidies are. In this case, those implicit subsidies come from regulation of the permitted methodologies to determine insurance premiums and any policies for mandatory natural catastrophe insurance in certain areas. Insurance not only benefits those who are affected by a disaster but, most crucially, makes costs associated with risk exposure and anticipated future risks transparent through premiums.

Thus, insurance is a valuable tool to promote climate change mitigation and adaptation at the individual, household, city, region, and even country levels. It is not as sexy as some new EV or CCS technology, but it scales faster and effectively aligns incentives regardless of political leanings.

California Sues Giant Oil Companies, Citing Decades of Deception

📰 Teaser: The state of California sued several of the world’s biggest oil companies on Friday, claiming their actions have caused tens of billions of dollars in damage and that they deceived the public by downplaying the risks posed by fossil fuels. Continue Reading → (5 min)

🤔 Moritz’ two cents: In short – nice, let’s hope something gets through. But I doubt that those lawsuits, even if successful, change the companies’ behaviour. I wonder what will. I hope it is a multitude of things, jurisdiction, policies, public pressure and last but not least, force from the financial markets and the shareholders. The last successful lawsuit I have heard, was a Dutch court obliging Shell to cut their emissions by 45 % by 2030 compared to 2019 in 2021. Shell is down from 60 million tons in 2021 to 51 million tons in 2022, but they also moved their headquarters from the Netherlands to the UK – for tax reasons, not to avoid jurisdiction though.

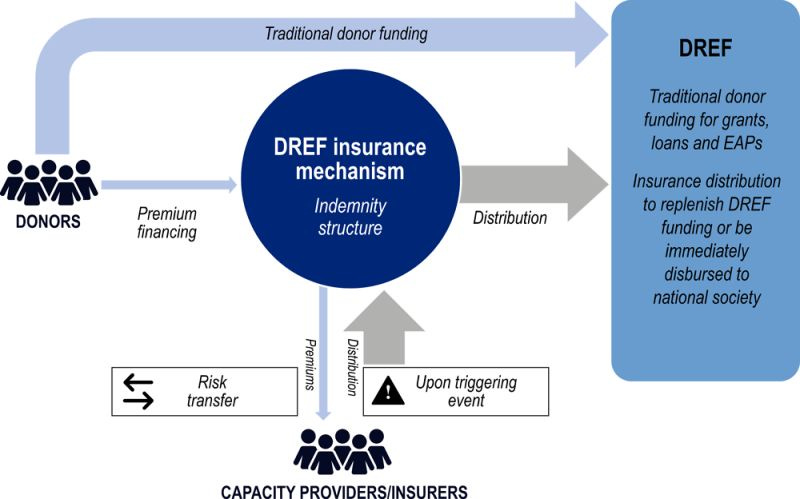

How to make climate disasters pay

📰 Teaser: The past few years have been unprecedented for the humanitarian sector. The escalating calamities and evolving crises occurring globally have demonstrated that, despite our utmost efforts, the presumptions, methodologies, and frameworks that have long defined humanitarian responses are no longer capable of adequately catering to the needs of individuals. The private sector has traditionally contributed to humanitarian budgets through grants with no expectation of return. However, the prospect of humanitarian responses becoming a new insurance market could change that perception. Continue Reading → (7 min)

(source: Jagan Chapagain (2023) - In my view: The untapped potential of innovative financing and humanitarian organisations)

🤔 Max’s two cents: Continued climate change makes climate disasters more frequent and increases their intensity, which puts enormous pressure on disaster response and humanitarian aid. From floods (Pakistan), droughts (Horn of Africa), to storms, there is a growing strain on global disaster relief support. While high-income countries tend to have sufficient resources to deal with such calamities, low-income countries depend heavily on the international aid sector, which in turn requires donations and grants by state, corporate, or private donors. Donations are not an ideal funding source, as willingness to contribute fluctuates, and media coverage of disasters matters greatly. This results in a funding gap that in 2022 of US$22.1 billion, set to increase in 2023.

Thus, using insurance products in disaster relief financing provides a promising new avenue. In the case of the Disaster Response Emergency Fund (DREF) by the International Red Cross and Red Crescent, donors do not pay into the fund itself directly, but instead pay the insurance premiums with their contributions. This leverages any contribution made to the extent of the payout once disaster strikes.

What further contributes to the effectiveness of such financing schemes is the use of parametric insurance instead of traditional insurance models. A parametric insurance has a set payout that is made once a trigger event, such as an earthquake, a minimum magnitude, or a certain amount of rain within a timeframe, is recorded. This setup allows for timely funding (especially relevant in humanitarian contexts) and reduces administrative burden since no damage assessment is necessary before payouts can be made, as is the case in common insurance models.

However, such funding structures also no silver bullet, as they are only applicable to cases where insurance companies can adequately model risks, where a suitable trigger event can be determined, and require significant effort while drafting the contract.

As you can probably guess by now, I am getting excited about different ways to use insurance to advance climate action, so expect some more insurance content going forward.

Blueprint for the future monetary system: improving the old, enabling the new

📰 Teaser: The BIS (Bank for international settlement) has published a new “Blueprint for the future monetary system: improving the old, enabling the new” in June. Mentioning this after Worldcoin in the last episode is… the contrary. It’s not by the people for the people, but by the bank to be used by everyone.

Key takeaways

• Tokenisation of money and assets has great potential, but initiatives to date have taken place in silos without access to central bank money and the foundation of trust it provides.

• A new type of financial market infrastructure – a unified ledger – could capture the full benefits of tokenisation by combining central bank money, tokenised deposits and tokenised assets on a programmable platform.

• As well as improving existing processes through the seamless integration of transactions, a unified ledger could harness programmability to enable arrangements that are currently not practicable, thereby expanding the universe of possible economic outcomes.

• Multiple ledgers – each with a specific use case – might coexist, interlinked by application programming interfaces to ensure interoperability as well as promote financial inclusion and a level playing field.

(→ Read the whole thing: 34 Pages)

🤔 Moritz’ two cents: The BIS proposes a fully centralized approach for the financial infrastructure by having “everything in one place”. A unified ledger. They later go on and continue that “The concept of a unified ledger does not mean “one ledger to rule them all” – a sole ledger that overshadows all other systems in the economy. Depending on the needs of each jurisdiction, multiple ledgers, each with a specific use case, could coexist.” So what good would it do? Centralized ledgers have single points of failure, data silos that can be controlled and seized by the one controlling the ledger and limited accessibility to everyone that the centralized party admits. The proposal could be understood as a proposal to keep power by controlling the data. It would still be the central party owning the data - not every individual citizen (you!). To give power to the people, don’t we want to reduce trust that is required?

Because trust can be breached. Institutional corruption or blindness is not uncommon. And the BIS has a history on that as well. Let’s quote a Harvard Ethics review on the early years of the BIS “Germany invaded Prague and Czechoslovakia ceased to exist. Three days later, the Reichsbank demanded the National Bank of Czechoslovakia order the gold in its BIS account transferred to Germany. They were also ordered to request the Bank of England transfer the 27 metric tons of gold in the National Bank of Czechoslovakia account there to Germany. The BIS transfer order went through,” LeBor writes. He adds that “Nazi Germany had just looted 23.1 metric tons of gold without a shot being fired.” (read more)

The BIS has been rebuilt since, so it is certainly better build and we do not know whether a decentral organisation could have done better. But we can give it a try.

📚 Rethink° Book Club

Please share with us what you are reading.

Moritz: A second round of Covid is on, it struck me down nicely, and I unfortunately finished the fantasy series Stormlight Archive (until the new book is published). So I went back to my non-fiction reading list: And the weak they suffer what they must by the ex-financial minister of Greece Mr. Varoufakis. It starts with a story about the origins of the Euro. It actually starts earlier, with how a beautifully designed monetary approach by Keynes (“Bancor” - Google it, it’s nice) lost in favour of Bretton Woods, how that got abandoned later and well, how it all lead up to the Euro. The most remarkable for me so far is a critique I have often been reading and that Varoufakis demonstrates by the foresight of Margaret Thatcher:

„Will the prime minister tell us,” asked one of Kinnock’s deputies, in misguided expectation that Thatcher would be discomfited by the subject, “if she will continue her personal fight against a single currency and an independent [European] central bank?” Before she could answer, another opposition deputy mischievously interjected, “She should be the governor!”

“What a good idea!” Thatcher replied after a great deal of merriment had filled the House. And then went on playfully to say, “I had not thought of it. But if I were, there would be no European central bank accountable to no one, least of all to national parliaments. Because under that kind of central bank there will be no democracy, [and the central bank will be] taking powers away from every single parliament and be able to have a single currency and a monetary policy and an interest rate policy that takes away from us all political power”

It was perhaps the first and last time a prime minister of a major European nation would hit the nail on the head regarding the nature of Europe’s monetary union. “

Max: This past month, I came across a book from my days as a master's student, “A Blueprint For A Safer Planet” by Nicholas Stern. I picked up the book at an event at LSE, where Mr. Stern presented his 2017 “Report of the high-level commission on carbon prices,” but I never read it. The book was published in 2009, so it is a bit dated in some aspects, but it largely seems to have aged well. The arguments for timely, decisive action remain relevant today, only that more frequent and extreme weather events have already manifested in the past years, and scientific methodologies can better model those. The book is a good introduction to economic approaches to tackling climate change, providing a deep dive into carbon tax and emission trading. Nevertheless, what most stuck with me was a short passage debunking the myth that a free-rider problem will undermine global climate action. This narrative is employed frequently, usually to justify delayed or curtailed climate action and to paint a dire picture of future climate action. There are three reasons why a free-rider problem might not occur, or at least occur merely to a manageable extent:

“First, many or most players are likely to worry that if they cheat, others may withdraw from the agreement, and the consequence of the “minor” increase in emissions will become major and very damaging increases globally.

Second, as agreement and action start to build, and new markets are created, the players seen to be irresponsible risk being excluded from key opportunities and major areas of future growth. An attempt to free-ride may prove costly for those who try.

Third, many participants will look beyond their own interest and worry about the consequences for all.”

Overall, the book paints a serious but not hopeless picture of the effort to mitigate climate change. While valuable years have gone by without sufficient climate action, there is still rational hope for action on every level, from the individual (mainly to drive system change), corporate, country, and global. Every tenth of a degree matters when it comes to limiting the harmful effects of climate change; thus the smallest action matters. What is important, however, is not to be content with a single incremental action (e.g., carbon pricing, carbon offsets, EVs, Carbon Capture and Storage solar, etc.) as there is no silver bullet solution.

Send us your recommendations, and we’ll list the highlights: me@mjmey.com

Not yet enough? Here are some evergreens and recent content we came across:

🗞️ The ESG on a Sunday newsletter is for everyone who wants to keep up with developments in sustainable finance.

🌍 Planet Critical is an excellent podcast for everyone who is into changing the world.

🎥 Water Bear is a non-profit movie platform focused on advancing activism, as a Netflix for impact.

📔 Any open questions on degrowth? You might find an answer in this book: “The political economy of degrowth” with 850+ pages by Timothée Parrique.

📅 Rethinking is timeless. Read the August issue.

Have you encountered something we might want to read/listen/watch? Please send it to us or leave a comment.

We hope you enjoyed it. Please comment, subscribe, and share.

All the best, and keep rethinking,